Founders pattern-match to a company they admire and pick the wrong business model. The saas vs marketplace decision (and the third option, e-commerce) is the highest-stakes architectural call of year one because the model decides stack, GTM motion, compliance load, and funding path. Pick wrong and the saas spends 18 months trying to be a marketplace while the marketplace tries to act like saas. Both fail.

This guide compares saas vs marketplace vs e-commerce across the four dimensions that actually matter: revenue primitives, unit economics, stack implications, and funding path. It includes the Revenue Primitive Map framework, payment plumbing decisions for each model, compliance loads founders typically miss, hybrid patterns that work, the switching cost when founders change their mind mid-build, and concrete examples from five Xgenious products that span the model spectrum.

Five takeaways before reading on: the four revenue primitives that define every business model, why marketplace unit economics differ fundamentally from saas, the Revenue Primitive Map for matching idea to model, the compliance gap that catches first-time marketplace founders, and the directional reality of model migration (saas to marketplace works rarely; marketplace to saas works often). For the broader build framework that places this decision in context, see how to build a saas in 2026.

Table of Contents

Saas vs Marketplace vs E-commerce: The Three Models in One Sentence

The three models, defined precisely:

Saas (software as a service). A software company sells access to a tool that the customer uses to do their own work. Revenue: recurring subscription fees per user, per seat, or per usage tier. Examples: Slack, Notion, HubSpot. Customer relationship: the company sells, the customer uses.

Marketplace. A platform connects two or more sides (typically supply and demand) and takes a cut of transactions facilitated. Revenue: take-rate (percentage of transaction value) or transaction fee (fixed per-transaction amount), often combined with subscription elements for premium features. Examples: Airbnb, DoorDash, Etsy. Customer relationship: the platform does not sell anything itself; it is the matchmaker.

E-commerce. A merchant sells physical or digital goods directly to end customers. Revenue: gross merchandise value (GMV) minus cost of goods sold (COGS) and fulfillment, with margin captured by the merchant. Examples: Warby Parker, Glossier, most Shopify stores. Customer relationship: the company is the seller of record, owns inventory or drop-ship relationships, ships the goods.

The confusion in saas vs marketplace conversations often comes from products that look similar on the surface. A “tool for finding freelancers” sounds like saas; if it takes a percentage of the freelance contract, it is a marketplace. A “platform for selling courses” sounds like a marketplace; if creators set their own prices and the platform charges them a flat monthly fee, it is saas with a thin commerce layer. The distinction is the revenue primitive, not the user experience. For the related question of saas vs web app within the saas category itself, see saas mvp vs web app.

Revenue Primitives: What Drives the Saas vs Marketplace Choice

Every business model collapses into one of four revenue primitives. The primitive determines unit economics, stack architecture, compliance posture, and funding path. Naming the primitive is the first step in any saas vs marketplace decision.

Primitive 1: Subscription. Recurring fixed fee per user or per tier. Predictable revenue, low billing complexity, high customer retention requirements. The native saas primitive. Lifetime value (LTV) calculated as monthly revenue × average customer lifespan, typically 24 to 60 months for B2B saas.

Primitive 2: Transaction fee. Fixed amount per transaction, regardless of transaction size. Common in payment processors, niche marketplaces, and high-volume commerce platforms. Revenue scales with volume independent of transaction value, which incentivizes the platform to drive transaction count over transaction size.

Primitive 3: Take-rate. Percentage of transaction value, typically 5 to 30 percent. The native marketplace primitive. Revenue scales with both volume and average transaction value. Marketplaces with high take-rates require high differentiation; commodity marketplaces compress to low single-digit take-rates over time.

Primitive 4: One-time. Single payment for ownership or perpetual access. The native e-commerce and traditional software-license primitive. Revenue is lumpy and forecasting is harder; LTV becomes a function of repeat purchase rate rather than retention rate.

Most products use one primary primitive plus one or two secondary ones. Saas often layers usage-based fees on top of subscription. Marketplaces often add subscription fees for sellers (Etsy Plus) or buyers (Amazon Prime). E-commerce often adds subscription elements (Dollar Shave Club, Glossier replenishment).

The dominant primitive determines the saas vs marketplace classification. A tool with subscription as 80 percent of revenue and transaction fees as 20 percent is saas. A platform with take-rate as 80 percent of revenue and subscription as 20 percent is a marketplace. The classification matters because it dictates everything downstream.

Saas vs Marketplace: Subscription Mechanics and Unit Economics

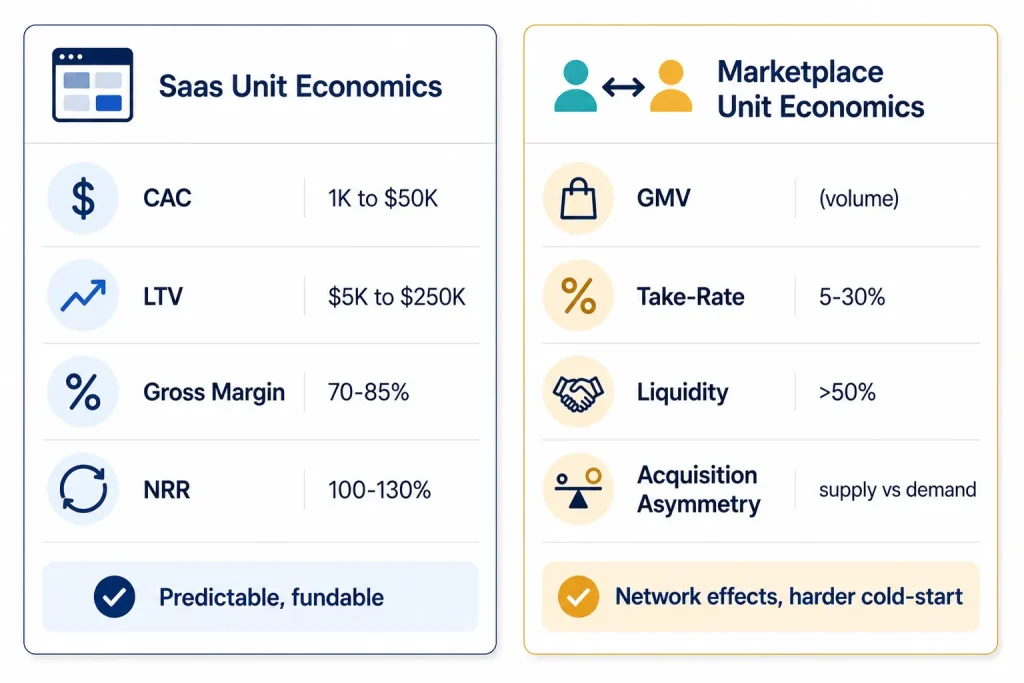

The saas model in 2026 is mature, well-instrumented, and well-funded. The unit economics are the most predictable of the three models in the saas vs marketplace comparison, which is why saas dominates venture capital allocation in software.

The core saas unit economics:

Customer Acquisition Cost (CAC). Sales and marketing spend divided by new customers acquired. Healthy B2B saas runs CAC around $1,000 to $5,000 for self-serve, $5,000 to $50,000 for sales-led mid-market, $50,000 to $500,000+ for enterprise.

Lifetime Value (LTV). Average revenue per customer multiplied by average customer lifespan. Healthy B2B saas runs LTV around 3x to 5x of CAC; below 3x is a sustainability problem, above 5x usually means under-investment in growth.

Gross margin. Revenue minus cost of revenue (hosting, support, third-party services). Healthy saas runs 70 to 85 percent gross margin, which is what makes the model attractive to investors.

Net Revenue Retention (NRR). Year-over-year revenue from existing customers, accounting for churn, downgrades, upgrades, and expansion. Healthy B2B saas hits 100 to 130 percent NRR; top-quartile hits 130 to 150 percent.

The reason saas dominates the saas vs marketplace funding conversation is unit economics: predictable CAC, high gross margin, recurring revenue that compounds. A saas at $1M ARR with 110 percent NRR and 75 percent gross margin gets funded easily; a marketplace at $1M GMV with 15 percent take-rate (effective $150K revenue) faces tougher questions despite the larger headline number.

The reason saas is hard despite the unit economics: customer acquisition is competitive, churn is brutal in undifferentiated categories, and the saas market in 2026 is saturated in most horizontal categories. Vertical saas (software for specific industries) is where the remaining greenfield exists.

Saas vs Marketplace: Take-Rate Math and Two-Sided Dynamics

Marketplaces look simpler than saas on paper and are dramatically harder to build in practice. The reason is two-sided dynamics: every marketplace has two distinct customer types (supply and demand) who must be acquired in coordination, and acquisition asymmetry kills more marketplaces than any other failure mode.

The core marketplace unit economics:

Gross Merchandise Value (GMV). Total transaction value flowing through the platform. Vanity metric on its own; meaningful only when paired with take-rate and gross margin.

Take-rate. Platform’s percentage of GMV. Ranges from 1 to 3 percent for commodity marketplaces (PayPal, eBay) up to 25 to 30 percent for high-differentiation marketplaces (Airbnb, DoorDash, Uber). The right take-rate is determined by what the platform can defend; under-priced take-rates leave money on the table, over-priced take-rates drive supply off the platform.

Liquidity. The probability that a request from one side gets matched by the other side within an acceptable time window. Liquidity is the single most important marketplace metric and the hardest to achieve. Below a threshold, the marketplace is “thin” and both sides churn; above the threshold, network effects compound and the marketplace becomes defensible.

The cold-start problem. Both sides need to be present for the marketplace to deliver value, but neither side has reason to join until the other is present. Solutions include single-side seeding (paying or subsidizing one side until liquidity exists), niche-then-expand (start in one geography or category, prove liquidity, expand), or productizing one side as a saas before adding the marketplace (the inverse hybrid pattern).

Acquisition asymmetry. One side is almost always meaningfully harder to acquire than the other. For freelance marketplaces, demand (clients) is hard; supply (freelancers) is easy. For lodging marketplaces, supply (hosts) is hard; demand (guests) is easy. Mistaking which side is hard burns marketing budget on the wrong side and stalls growth for quarters.

The benchmarks for marketplace unit economics differ fundamentally from saas. The canonical reference is a16z’s marketplace metrics framework, which covers GMV, take-rate, liquidity, and repeat behavior. For the platform-economics theory underlying marketplace dynamics, Sangeet Paul Choudary’s work is the standard reference.

In 2026, marketplace funding requires a higher bar than saas in the saas vs marketplace investor conversation: clear evidence of liquidity in a defined market, a take-rate the supply side accepts, and a path to network effects strong enough to defend against horizontal competitors. Most pre-seed marketplace founders should validate at least one geography or vertical to liquidity before raising; raising on hypothetical liquidity has a much lower success rate in 2026 than in 2018.

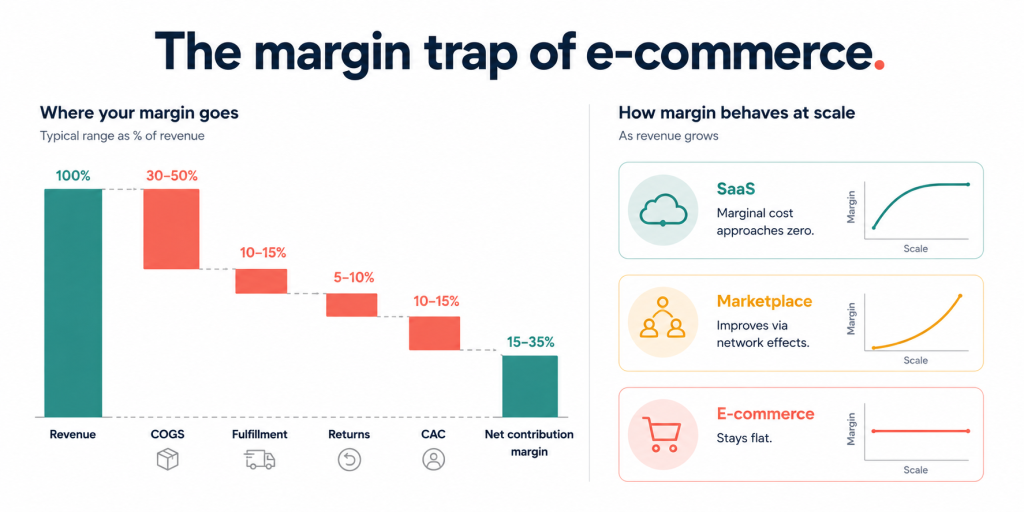

Saas vs Marketplace vs E-commerce: The Margin Trap of E-commerce

E-commerce is the third model in the saas vs marketplace conversation and the one founders most often misunderstand. E-commerce looks like saas in marketing copy (“subscribe to weekly deliveries”) and like a marketplace in operations (inventory, fulfillment, returns), but the unit economics are fundamentally different from both.

The core e-commerce unit economics:

Gross margin after COGS. Revenue minus cost of goods sold. Direct-to-consumer (DTC) brands typically run 50 to 70 percent gross margin pre-fulfillment, but fulfillment, returns, and customer service drive net contribution margin down to 15 to 35 percent in most categories.

Customer Acquisition Cost (CAC) vs. average order value (AOV). E-commerce CAC has risen sharply since 2020 (post-iOS 14, post-Meta ad targeting changes). Healthy DTC requires AOV to be 3 to 5 times CAC, ideally with high repeat purchase rates to push LTV/CAC above 3x.

Inventory carrying cost. Capital tied up in inventory that has not yet sold. The hidden cost of e-commerce that founders consistently underestimate. A DTC brand with $1M in inventory and 90-day inventory turn is sitting on roughly $250K in working capital that does not earn returns.

Returns and refunds. Apparel and footwear see 20 to 40 percent return rates; electronics see 8 to 15 percent. Returns destroy margin because the cost of return shipping, restocking, and damaged inventory is rarely fully recovered.

The illusion of scale in e-commerce: revenue grows with order volume, but margin does not improve at the same rate because COGS, fulfillment, and CAC scale roughly linearly. Saas margins improve dramatically with scale (the marginal cost of an additional user approaches zero); marketplace margins improve at scale through network effects; e-commerce margins do not improve much without dramatic supplier renegotiation or vertical integration.

The reason e-commerce raises less venture capital than saas or marketplaces in 2026: the unit economics ceiling is lower and harder to break. E-commerce raises tend to be smaller, with debt and inventory financing playing larger roles than equity. Founders deciding between saas vs marketplace vs e-commerce should understand that the funding path for e-commerce is fundamentally different from the other two.

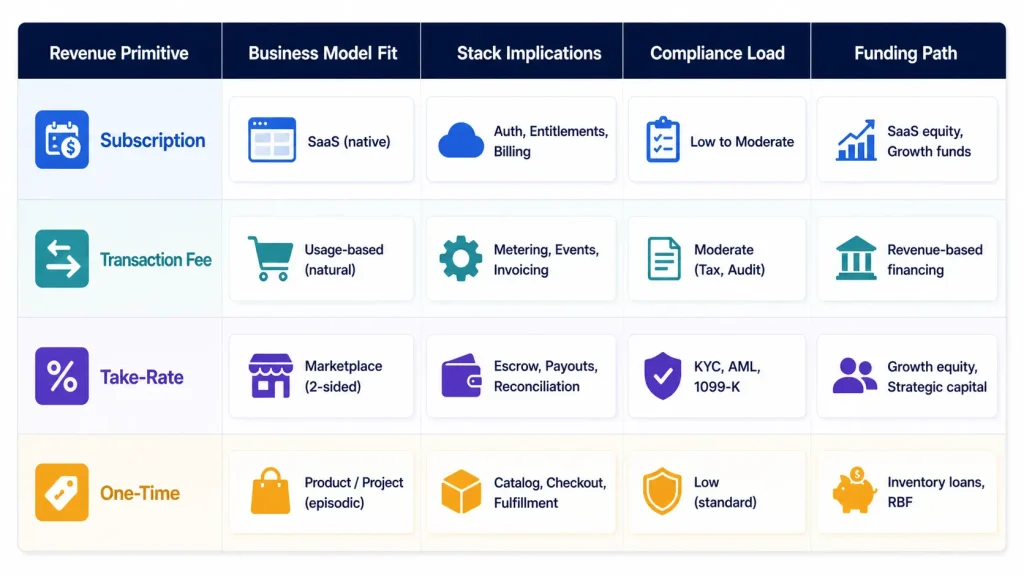

The Revenue Primitive Map: A Saas vs Marketplace Framework

The Revenue Primitive Map is the framework this article is built around. It maps the four revenue primitives (subscription, transaction fee, take-rate, one-time) to four dimensions that determine whether a model fits a particular idea.

The four mapped dimensions:

Dimension 1: Business model fit. Which primitives match which business models. Subscription maps cleanly to saas, weakly to marketplace (premium features). Take-rate maps cleanly to marketplace, weakly to saas (rare). Transaction fee maps to commerce-adjacent saas and high-volume marketplaces. One-time maps to e-commerce and traditional software.

Dimension 2: Stack implications. What infrastructure each primitive demands. Subscription requires Stripe Billing or equivalent (proration, dunning, tax). Take-rate requires Stripe Connect or similar marketplace payments (split payments, payouts, KYC). Transaction fee requires reliable per-transaction logging and reconciliation. One-time requires checkout, fulfillment integration, and refund handling.

Dimension 3: Compliance load. What regulatory work each primitive triggers. Subscription is the lightest (sales tax, consumer protection). Take-rate is the heaviest (KYC for both sides, money transmission licensing in some jurisdictions, 1099-K reporting for US sellers, AML compliance). One-time e-commerce sits in between (sales tax, consumer protection, return regulations).

Dimension 4: Funding path. Which primitives unlock which capital sources. Subscription saas attracts the broadest VC pool because the unit economics are predictable. Marketplace VCs are a smaller specialized pool with higher diligence on liquidity. E-commerce typically raises through revenue-based financing, inventory loans, and smaller equity rounds.

The Map is used backwards. Start with the idea, identify what the user is paying for, identify the primitive, then read the implications across all four dimensions. The wrong primitive choice in a saas vs marketplace decision produces an architecture that does not fit the business model, a compliance posture that is either over-engineered or under-engineered, and a funding path that the team cannot actually walk.

The downloadable Revenue Primitive Map template is included at the end of this article.

Payment Plumbing for Saas vs Marketplace: Stripe Billing vs Connect vs Shopify

Payment plumbing varies dramatically across the saas vs marketplace divide. The wrong payment platform locks the saas into months of rebuild work when the model evolves.

Stripe Billing. The default for saas. Handles recurring subscriptions, proration, dunning, plan changes, tax (with Stripe Tax). Rolling a custom billing system instead of using Stripe Billing is the second-fastest way to burn a seed round. Charges 2.9 percent + 30 cents per transaction in the US, with subscription features bundled.

Stripe Connect. The default for marketplaces. Handles split payments (platform takes a cut, supply side gets paid out), KYC for connected accounts, payout scheduling, 1099-K generation for US tax compliance. The Stripe Connect documentation covers the patterns: Standard accounts (the connected user has a Stripe account), Express accounts (Stripe-managed onboarding), and Custom accounts (the platform handles all UX). Most marketplaces in 2026 use Express accounts as the right balance of control and onboarding speed.

Shopify (and Shopify Plus). The default for e-commerce. Handles inventory, checkout, payment processing, fulfillment integrations, customer accounts, marketing tools. Not a payment processor in the same sense as Stripe; Shopify is a full e-commerce stack with payment as one component. Shopify charges 2.9 percent + 30 cents per transaction (similar to Stripe) plus monthly platform fees ($79 to $399 for Shopify, $2,000+ for Plus).

The cross-over cases. A saas that adds a marketplace component (Stripe Billing for subscription, Stripe Connect for the marketplace) ends up running both Stripe products simultaneously, which is fully supported but adds operational complexity. An e-commerce business that adds saas-like subscriptions (Glossier replenishment, Dollar Shave Club) typically uses Shopify Subscriptions or Recharge, layered on top of Shopify.

The hidden cost of getting payment plumbing wrong in the saas vs marketplace stack decision: a saas that picked Stripe Billing and later wanted to add a marketplace must integrate Stripe Connect from scratch, which is roughly 4 to 8 weeks of work plus KYC/AML compliance review. A marketplace that picked Stripe Connect and later wants to layer saas subscriptions has the easier path because Connect supports subscription billing on connected accounts.

Stack Implications of Saas vs Marketplace: Why Architecture Diverges

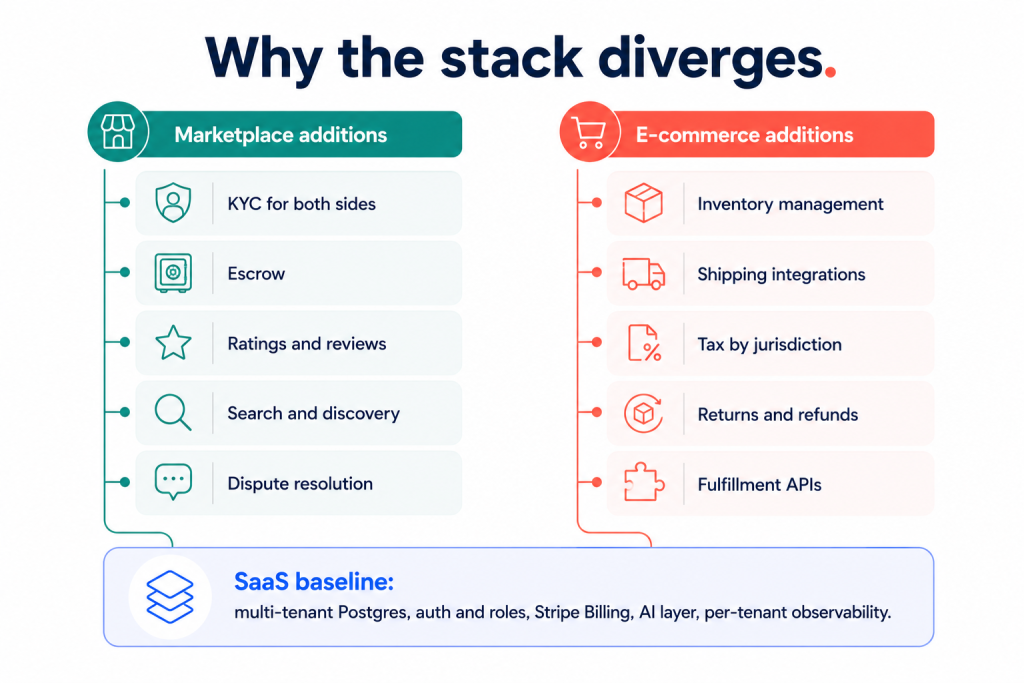

The stack implications of saas vs marketplace decisions fork at the data model. A saas application stores customers, users, and the data those users create. A marketplace stores supply listings, demand requests, transactions, payouts, and the matching logic between sides. The data model difference cascades through every layer of the stack.

Saas stack baseline. Multi-tenant Postgres with row-level security, auth provider with team and role management, billing integration with Stripe Billing, AI layer for product features, observability tagged per tenant. Discussed in depth in the 2026 saas tech stack.

Marketplace stack additions. Beyond the saas baseline, the marketplace side of the saas vs marketplace stack equation requires: identity verification (KYC) for both sides at signup or first transaction, escrow logic to hold funds between transaction acceptance and completion, rating and review systems for both sides, search and discovery infrastructure (often Algolia, Typesense, or Elasticsearch), notification systems supporting near-real-time updates between sides, and dispute resolution workflows.

E-commerce stack additions. Beyond the saas baseline, e-commerce requires: inventory management (real-time stock counts, reservation logic during checkout), shipping integrations (rate calculation, label generation, tracking), tax calculation that varies by destination jurisdiction, returns and refund workflows, fulfillment provider integrations (warehouse management, drop-shipping APIs).

The architectural cost difference is real. A saas MVP ships in 8 to 12 weeks at $25K to $80K. A marketplace MVP requires 12 to 20 weeks at $40K to $150K because of KYC, escrow, search, and dispute systems that have no saas equivalent. An e-commerce MVP often ships fastest if built on Shopify ($79 per month plus theme work), but custom e-commerce that needs unique inventory or fulfillment logic costs as much as a marketplace MVP.

The pattern that breaks founders in the saas vs marketplace stack decision: starting a marketplace MVP on a saas-shaped budget. The KYC, escrow, and search components alone consume 30 to 50 percent of build time, which the saas budget did not account for. Founders who start a marketplace expecting saas-build economics end up with half a marketplace and no money left to finish.

Compliance Load by Model in Saas vs Marketplace

Compliance load varies more than founders expect across saas vs marketplace vs e-commerce. Each model triggers a different regulatory surface area.

Saas compliance load. GDPR for any saas with EU users, SOC 2 Type II for enterprise sales above $50K ARR, HIPAA only for healthcare PHI, sales tax (Stripe Tax handles most cases), consumer protection in some jurisdictions. Total compliance work at MVP stage: 2 to 4 weeks of architectural setup, $5K to $20K in legal review, $20K to $40K for SOC 2 once justified.

Marketplace compliance load. Heavier across the board. Beyond saas requirements, marketplaces add: KYC for supply-side users (mandated by payment processors, often by law in financial services), AML compliance for transaction monitoring, money transmission licensing in some jurisdictions if the platform holds funds for more than a brief settlement window, 1099-K reporting for US sellers (tax form generation for US sellers who clear the federal 1099-K threshold, restored to $20,000 and 200 transactions for 2026 by the 2025 One Big Beautiful Bill Act, with several states setting lower thresholds), seller agreements with terms binding both sides, and consumer protection enforcement when transactions go wrong.

Total marketplace compliance work: 6 to 12 weeks of architectural and legal setup, $20K to $60K in legal review for US-only operation, significantly more for cross-border.

E-commerce compliance load. Sales tax compliance across jurisdictions (every state in the US has its own rules, simplified by Shopify or TaxJar but still real work), product liability for any physical goods, return and refund regulations (varying by jurisdiction, particularly strict in EU), data privacy for customer accounts (GDPR, CCPA), and category-specific regulations (FDA for cosmetics and supplements, alcohol licensing, age verification for restricted products). Total e-commerce compliance work: 4 to 8 weeks of setup, $10K to $30K in legal review.

The hidden compliance cost in saas vs marketplace decisions: marketplace compliance is ongoing work, not a one-time setup. Every new jurisdiction the marketplace serves adds compliance overhead. Every new regulation (digital services taxes in EU, gig worker classification rules in US, payment regulation in Asia) requires updated terms, updated KYC, and sometimes updated technical implementation. Marketplace founders should budget 5 to 10 percent of engineering time on ongoing compliance maintenance, not just the initial setup.

Funding Path in Saas vs Marketplace: Which Raises Easier in 2026

The funding path differs substantially across saas vs marketplace vs e-commerce in 2026. Understanding which capital sources align with which model prevents founders from chasing the wrong investor pool.

Saas funding path. The broadest VC pool. Pre-seed checks of $250K to $1.5M, seed of $1M to $5M, Series A of $5M to $20M, with the unit economics expectations rising at each round (ARR thresholds, NRR thresholds, gross margin thresholds). Saas-specialist VCs are abundant; generalist VCs understand saas economics; banks lend against ARR through revenue-based financing and venture debt.

Marketplace funding path. A smaller, more specialized VC pool. Marketplace investors at the seed stage want to see clear evidence of liquidity in at least one geography or vertical, a defensible take-rate, and a path to network effects. Pre-seed for marketplaces is harder than saas because the cold-start problem makes early traction harder to demonstrate. The marketplace VCs who fund successfully (NfX, Andreessen Horowitz, Bessemer, Bond) write fewer checks than saas VCs at comparable stages.

E-commerce funding path. Smallest equity pool, largest debt pool. E-commerce raises in 2026 are increasingly debt-financed: revenue-based financing through Pipe, Capchase, or Stenn; inventory loans through Wayflyer or Clearco; merchant cash advances for short-term working capital. Equity rounds for DTC brands have shrunk meaningfully since the 2021 peak, and the bar for “interesting to VCs” has risen to roughly $5M ARR with strong unit economics.

The funding implication of the saas vs marketplace decision is real: choose saas if the team intends to raise institutional VC and has no specific reason to be a marketplace. Choose marketplace deliberately, knowing that the funding path is harder and the diligence is sharper. Choose e-commerce knowing that the equity path is narrow and the debt path is the more common scaling route.

The cross-cutting reality in the saas vs marketplace funding conversation: hybrid models that combine saas subscription with marketplace take-rate often raise easier than pure marketplaces because the subscription component anchors predictable revenue. Toast, Square, and several vertical saas-marketplace hybrids have demonstrated this pattern.

Hybrid Models: When Saas vs Marketplace Becomes Saas Plus Marketplace

The most interesting evolution in saas vs marketplace decisions in 2026 is the hybrid pattern: products that combine saas subscription with marketplace take-rate, capturing the predictable revenue of saas and the network effects of marketplace.

The directionality of model evolution matters. Marketplaces becoming saas works often because the marketplace already has supply and demand engaged, and adding subscription tools (analytics, marketing, premium features) is incremental work for the existing audience. Toast started as a payment terminal for restaurants, added saas tools (online ordering, payroll, gift cards), and now generates more revenue from subscription than from payments. Square followed a similar pattern.

Saas becoming marketplace works rarely because the saas customer base is one side of a potential marketplace, and acquiring the other side is the same cold-start problem any marketplace faces. Slack tried to build an app marketplace; the participation never reached the threshold needed for true network effects. Notion attempted templates as a marketplace surface; the supply side existed but the demand side largely consumed the templates as features rather than as marketplace transactions. The successful saas-to-marketplace transitions usually happen when the saas already has both sides as users and the marketplace layer formalizes existing behavior.

The three working hybrid patterns in 2026:

Pattern 1: Saas with embedded marketplace. The saas tool includes a curated marketplace of integrations, services, or templates. Revenue mostly subscription, with marketplace as a customer-acquisition or retention surface. Example: HubSpot solutions partner directory.

Pattern 2: Marketplace with saas tier for power users. The marketplace provides core matching for free or low fee, charges supply-side users for productivity tools (analytics, automation, premium listings). Revenue split between take-rate and subscription. Example: Etsy Plus, Upwork’s Plus Tier.

Pattern 3: Vertical saas with payments embedded. A vertical saas (industry-specific) adds payment processing as a revenue line, charging interchange-plus or fixed take-rate on transactions processed. Revenue heavily weighted to payments at scale. Example: Toast, ServiceTitan, Mindbody.

The hybrid pattern is increasingly the right answer in vertical categories where the saas captures the workflow and the marketplace captures the transactions. Founders building in restaurant tech, service businesses, healthcare, or trade industries should consider hybrid models from day one rather than picking saas vs marketplace as a binary.

Five Xgenious Examples Across the Saas vs Marketplace Spectrum

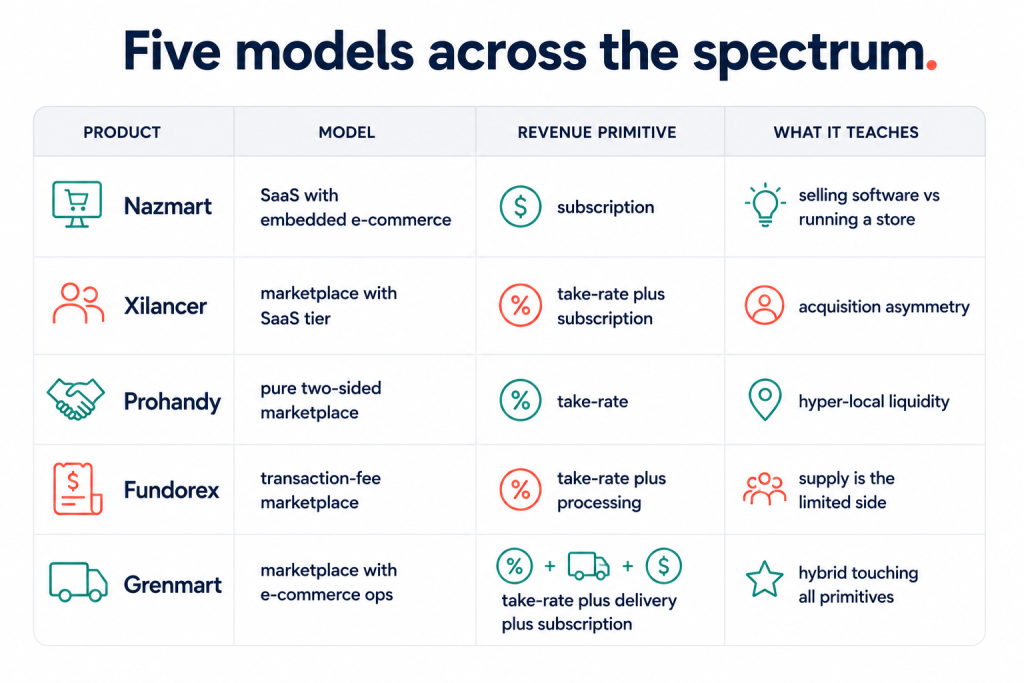

Five products in the Xgenious portfolio span the saas vs marketplace spectrum and demonstrate what each model looks like in production. Each is examined for what it teaches about its model, not as a feature pitch.

Nazmart (eCommerce SaaS). A multi-tenant platform that lets merchants run their own e-commerce stores. Revenue: subscription per merchant. Model: saas with embedded e-commerce. Teaches: the difference between selling e-commerce software (saas, predictable) versus running an e-commerce business (one-time revenue, lumpy). Nazmart’s tenants run e-commerce; Nazmart itself is saas. Conversion benchmarks: standard saas trial-to-paid (15 to 25 percent for B2B sales-led). For the productized platform, see Nazmart.

Xilancer (freelance marketplace). A platform connecting freelancers (supply) with clients (demand). Revenue: take-rate on contract value plus subscription tiers for premium features. Model: marketplace with saas tier. Teaches: acquisition asymmetry in freelance marketplaces. Supply (freelancers) is easy to acquire; demand (clients with budget and clear briefs) is hard. The difficult side determines the marketing budget. For the productized platform, see Xilancer.

Prohandy (on-demand services). A two-sided marketplace connecting service providers (supply) with consumers (demand) for on-demand home services. Revenue: take-rate plus optional subscription for service providers. Model: pure two-sided marketplace. Teaches: hyper-local liquidity matters more than global. A marketplace with 1,000 providers across 10 cities is liquid in zero cities; the same 1,000 providers in one city is liquid. For the productized platform, see Prohandy.

Fundorex (crowdfunding). A platform connecting backers with project creators. Revenue: take-rate on funded projects plus payment processing fees. Model: transaction-fee marketplace. Teaches: marketplace dynamics where supply is the limited side and demand is broad. The platform spends most of its acquisition budget on supply (project creators with credibility), not demand.

Grenmart (grocery commerce). A multi-vendor grocery marketplace combining marketplace mechanics with e-commerce operations. Revenue: take-rate on vendor sales plus delivery fees plus subscription for vendor tools. Model: marketplace with e-commerce operational layer. Teaches: hybrid models that touch all three primitives, with the operational complexity that comes with combining them.

The pattern across all five Xgenious examples in the saas vs marketplace spectrum: the model determines the unit economics, the stack, the compliance load, and the funding path. Mixing them up costs months. The portfolio exists in part to demonstrate that all three model types are buildable on a common compliance-ready, multi-tenant architectural foundation, but with model-specific layers stacked on top. For the broader build framework, see how to build a saas in 2026.

The Switching Cost in Saas vs Marketplace Decisions

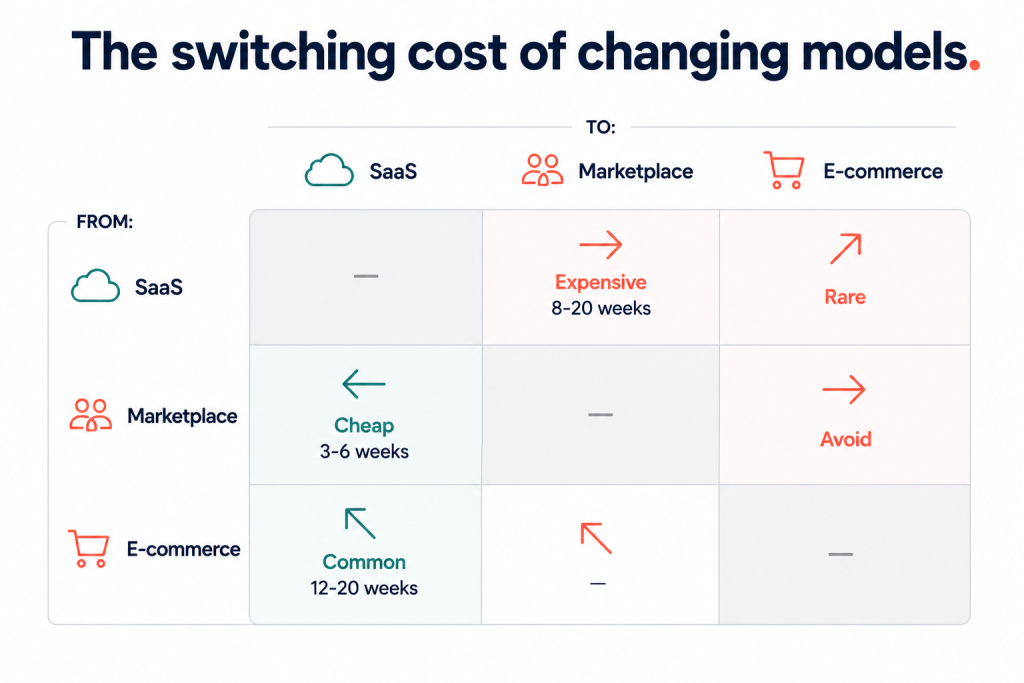

The switching cost of changing models mid-build is meaningful and asymmetric. Understanding which transitions are cheap and which are expensive prevents founders from making the wrong call early in the saas vs marketplace decision.

Saas to marketplace. Expensive. Adding a marketplace layer to an existing saas requires KYC infrastructure, Stripe Connect integration, escrow logic, search and discovery, and dispute resolution. Roughly 4 to 8 weeks of additional engineering plus 4 to 12 weeks of legal and compliance setup. The cold-start problem also reappears: the existing saas customers may not be the right “supply” or “demand” for the new marketplace layer.

Marketplace to saas. Cheaper. Adding subscription features to an existing marketplace usually means adding Stripe Billing alongside Stripe Connect, building feature flags for premium tiers, and shipping the saas-style features (analytics, automation, premium listings) to existing supply or demand-side users. Roughly 3 to 6 weeks of engineering. The existing audience is the customer base, removing the cold-start problem.

Saas to e-commerce. Rare. Saas companies that pivot to selling physical goods typically do so to monetize an existing audience (Glossier from Into the Gloss media, MeUndies from a content brand). The pivot is more about brand and inventory than software architecture; the saas itself usually does not become the e-commerce platform.

E-commerce to saas. Increasingly common. DTC brands that built operational tooling for themselves (Glossier’s customer service workflows, Allbirds’ supply chain tools) sometimes spin those tools out as saas products for other DTC brands. The transition requires re-architecting internal tooling for multi-tenant use, which is roughly 12 to 20 weeks of work.

Marketplace to e-commerce. Avoid. A marketplace operator who tries to vertically integrate by sourcing inventory and selling directly often loses the marketplace flywheel without building competitive e-commerce operations. Amazon’s hybrid is the exception, not the pattern.

The switching cost guidance for the saas vs marketplace decision: pick deliberately at the start, but build with model-aware foundations (Stripe Billing supports later Connect integration, multi-tenant Postgres supports both pure saas and marketplace data shapes) so that selective evolution is possible without full rebuilds.

Conclusion: The Saas vs Marketplace Decision as the First Architectural Call

The saas vs marketplace vs e-commerce decision is the highest-stakes architectural call of year one. Three models, four revenue primitives, four mapped dimensions (business model fit, stack, compliance, funding path). The Revenue Primitive Map makes the saas vs marketplace decision systematic rather than instinctive. The Xgenious portfolio demonstrates all three models in production, with model-specific layers stacked on a common compliance-ready foundation.

The dominant 2026 default for software founders without a specific reason to be a marketplace or an e-commerce business is saas: predictable unit economics, broadest VC funding pool, lightest compliance load, fastest validation cycle. The right reason to choose marketplace is genuine two-sided dynamics where transaction value scales with both sides being present. The right reason to choose e-commerce is owning the product or category in a way software cannot.

Hybrid models (saas with marketplace layer, marketplace with saas tier, vertical saas with payments) are increasingly the most defensible 2026 patterns. Build the foundation generically (multi-tenant, Stripe Billing-compatible, KYC-ready architecture) so the model can evolve from a clean starting position when the market signals a hybrid opportunity.

Saas vs Marketplace FAQ

1. Can I start as saas and add a marketplace later?

Possible but expensive. Adding a marketplace layer to a saas requires roughly 4 to 8 weeks of engineering plus 4 to 12 weeks of legal and compliance setup. The cold-start problem also reappears in the saas vs marketplace evolution path: existing saas customers may not be the right two sides for the new marketplace. The cleaner path: if a marketplace is in the long-term plan, build the saas with marketplace-ready primitives (Stripe Billing alongside Connect-compatible architecture) from day one, then activate the marketplace layer when liquidity in a specific market is proven.

2. Which model is cheapest to validate?

Saas, by a meaningful margin. A saas idea can be validated through 20 conversations and a fake-door landing page in 30 days for under $2K. A marketplace requires validating both sides of the market separately, which doubles the validation cost and timeline. E-commerce validation requires actual inventory or pre-orders, adding inventory cost to validation budget. The order of validation cost from cheapest to most expensive in the saas vs marketplace comparison: saas, e-commerce (with pre-sells), marketplace.

3. Which model is hardest to fund?

E-commerce by equity, marketplace by diligence depth. E-commerce equity rounds have shrunk significantly since the 2021 peak; most e-commerce raises are debt-financed in 2026. Marketplaces face the highest diligence bar at seed stage because investors want proof of liquidity in a defined market before writing checks. Saas remains the easiest of the three to raise institutional equity for, assuming standard unit economics.

4. How do I know if my idea is a marketplace in disguise?

Three signs in the saas vs marketplace classification check. First, the value proposition involves connecting two distinct user types (sellers and buyers, providers and customers, hosts and guests). Second, revenue scales with transaction volume between users, not with subscription tiers. Third, the team finds itself worrying about both sides of the market, not just acquiring one customer type. If all three are present, the idea is a marketplace regardless of how the founder describes it.

5. Can one product be all three?

Rarely well. Hybrid models that combine two primitives (saas + marketplace, marketplace + e-commerce) work when one model is dominant and the other is a complementary layer. Trying to be all three at once typically produces operational complexity without clear positioning. Most successful “all three” companies (Amazon, Shopify Plus, Toast) reached that state by mastering one model first and adding others over years, not by launching all three at once.

6. Does a marketplace need a supply-side app?

Usually yes for service marketplaces, optionally for product marketplaces. Service marketplaces (Prohandy-style on-demand services, freelance platforms with active project work) require supply-side mobile apps because providers work in the field, accept jobs in real time, and need notifications. Product marketplaces (Etsy, Amazon) work with web-only supply-side interfaces because sellers manage inventory at desks, not on the move. The need for a supply-side app adds roughly 8 to 12 weeks and $30K to $80K to the marketplace MVP build.